Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

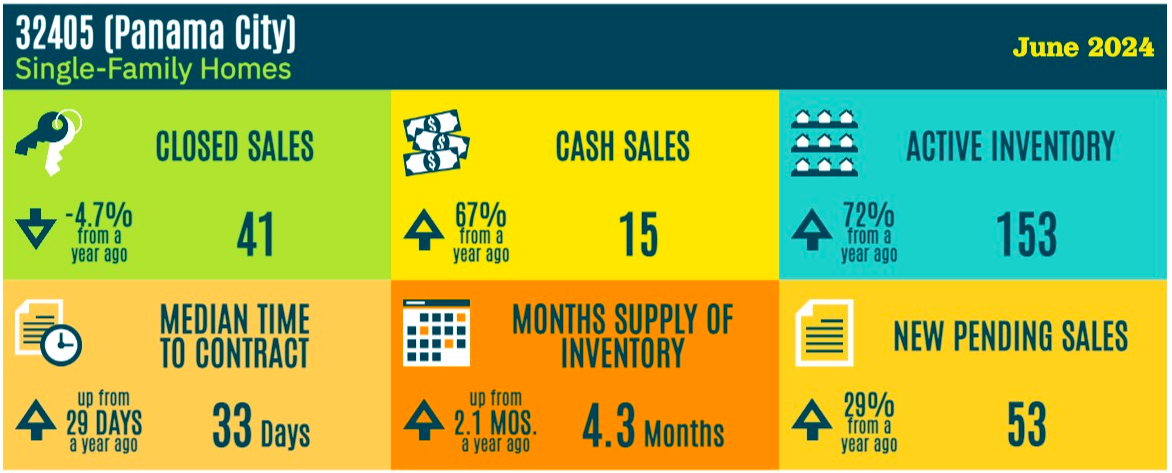

I get asked all the time about real estate in NW Florida, so I thought I’d share my opinion on what’s to come for the rest of the 2024 year, and into 2025.

🚨The housing market is dynamic and influenced by various factors, including interest rates. Many experts predict a potential market resurgence if interest rates decline in #September2024, leading to increased home prices, all consumers fighting multiple offers, and a reduction on inventory.

If you’re a #homeowner considering selling: 🏡

Prepare your home now: Begin decluttering and making necessary repairs to maximize its appeal to potential buyers.

Time your listing: Carefully consider market conditions and consult with me to determine the optimal time to list your property.

TO DO CHECK LIST for Property Owners: Curb appeal, Declutter, Deep clean forgotten areas, Make obvious repairs, Don’t make excessive improvements, Buy new light bulbs, Clear off surfaces, !CLEAN clean CLEAN!, Neutralize your walls, Paint the walls, Remove odors, Move out if you can, Market your home effectively with Video and Pro-Photos (your awesome realtor should be doing this for you), Price your home competitively (your awesome realtor should be providing you with recent COMPS), Estimate your net proceeds (your awesome realtor should be aiding with all your TITLE needs), lastly, Can you offer Mortgage Assumption, or Seller Financing?

If you are on the consumer side:🏡

Evaluate your financial situation: Determine your budget, desired timeline, and long-term #goals. Consider current market conditions: Weigh the pros and cons of buying now versus waiting, including potential interest rate fluctuations and their impact on affordability. Explore refinancing options: If you purchase a home now and interest rates decrease later, refinancing could potentially lower your monthly mortgage payment. Remember, the housing market is complex. Consulting with a financial advisor and schedule an appointment with me, (your family go-to real estate professional) and together we can provide personalized guidance based on your specific circumstances. Speak to mortgage companies to find the best program that fits your needs.

How interest rate cuts could lower monthly mortgage costs

Most major housing organizations expect mortgage rates to drop by the end of the year. And they’ve already gone down from 7% to 6.87% in the past week, according to the Mortgage Bankers Association.

Mortgage rate forecasts for the end of 2024 differ slightly. Realtor.com expects average rates to fall to 6.5%, while Fannie Mae predicts 6.7%.

There might be more breathing room in 2025, too, as major forecasts expect rates to continue to slide. Wells Fargo forecasts APRs to average 6% in the first three months of 2025, while the MBA expects a rate of 5.9%.

- 6.87% (current): $2,210

- 6.7%: $2,172

- 6.5%: $2,128

- 6%: $2,018

- 5.9%: $1,997

Yes, you can refinance a government loan such as an FHA, VA, or USDA loan to a conventional loan. Refinancing to a conventional loan can be an effective way to access savings by removing mortgage insurance or mandatory fees that are common with government-backed loans.

By refinancing to a conventional loan, in addition to potentially lowering your interest rate, reducing your monthly payment, gaining access to your home equity (through a cash-out refinance), or adjusting your loan term, you could also:

- Avoid the mandatory mortgage insurance premium (MIP) from your FHA loan.

- Avoid the VA funding fee or use the home you purchased with a VA loan to earn rental income.

To be approved for a conventional loan you must meet these additional qualifying requirements:

- Wait 210 days or have made at least 6 monthly payments to refi from an FHA or VA loan.

- Have at least 3% home equity before you can refinance from a USDA loan.

-

Conventional loan refinance

Homeowners with VA or USDA loans may need to meet additional criteria to refinance to a conventional loan. For example, VA loan holders may need to wait 210 days or make six monthly payments before refinancing, while USDA loan holders may need to have at least 3% home equity.

-

VA streamline refinance

Also known as an interest rate reduction refinance loan (IRRRL), this type of refinance can help lower interest rates or convert an adjustable-rate mortgage (ARM) to a fixed-rate mortgage. To qualify, borrowers must have an existing VA-backed home loan, certify that they currently or previously lived in the home, and have a mortgage payment history with no more than one late payment in the last 12 months. VA streamline refinance guidelines also state that income, assets, credit, and employment do not need to be verified, and home appraisals are usually not required.

-

USDA loan refinanceBorrowers must have had the existing USDA loan for at least 12 months and their mortgage must be current for the last 180 days. They must also have a low to median income, with a household income limit of $103,500 for a family of 1-4 in most of the U.S. as of 2023. Income limits apply to everyone living in the home and receiving income, even if they aren’t listed on the loan application. The refinanced home must also be the borrower’s primary residence.

#Disclaimer: This information is intended for general knowledge and informational purposes only, and does not constitute financial advice. It’s crucial to conduct thorough research and consult with professionals like financial advisors and your family before making any #realestate decisions.

💻👱♀️📲Happy to help! (850) 896-2487 ❤️